Thanks to my friends at Melio for sharing this article.

Global work is just work now. Your clients are not only hiring talent across borders; they’re transacting with vendors and contractors in multiple currencies as a routine part of how their businesses operate.

As a result, many accounting leaders are asking the same question right now - both for their own firms and for the clients they advise: What’s actually the best way to handle international payments and foreign exchange (FX)?

Part of the issue is that most firms haven’t landed on a clean solution for their own international payments. So you’re figuring it out for yourself at the same time as you’re managing it for clients, and the complexity compounds.

Business owners have normalized the friction. They’re not asking for a better setup because they don’t know one exists. But you’re in a position to see it clearly for both of you — and that’s where the opportunity sits.

First, a distinction:

The terms “international payment” and “foreign exchange (FX) payment” are often used interchangeably, but there’s an important distinction worth making.

International payment is the umbrella term for any money movement across borders, regardless of currency.

Within that, there are two approaches: you can send USD as-is, so the recipient gets dollars; or you can make an FX payment, where the currency is converted at the point of transaction. Your client’s account is debited in USD, but the vendor receives payment in their local currency.

Contractors and vendors almost always prefer local currency, and for good reason. When payments are sent in USD internationally, vendors can be hit with surprise fees or unfavorable exchange rates on their end, meaning they receive less than expected. That creates friction, erodes trust and puts your client in the awkward position of explaining a shortfall they didn’t cause.

FX payments, by converting the currency upfront, remove that uncertainty.

The vendor knows exactly what they’ll receive, and your client has full visibility into the true cost. Most firms, however, aren’t making a deliberate choice between the two - they’re managing whatever setup they’ve accumulated.

Most firms fall into a messy process without meaning to.

A client brings on an overseas contractor, so you find a way to pay them. A supplier wants to be paid locally, so you add a platform for that. Another client is already using something else and wants to stay on it, so you work with that too.

Each decision makes sense in the moment. Over time, they accumulate, and you end up managing international payments across multiple systems, with inconsistent data and no simple way to see the total cost without recalculating it.

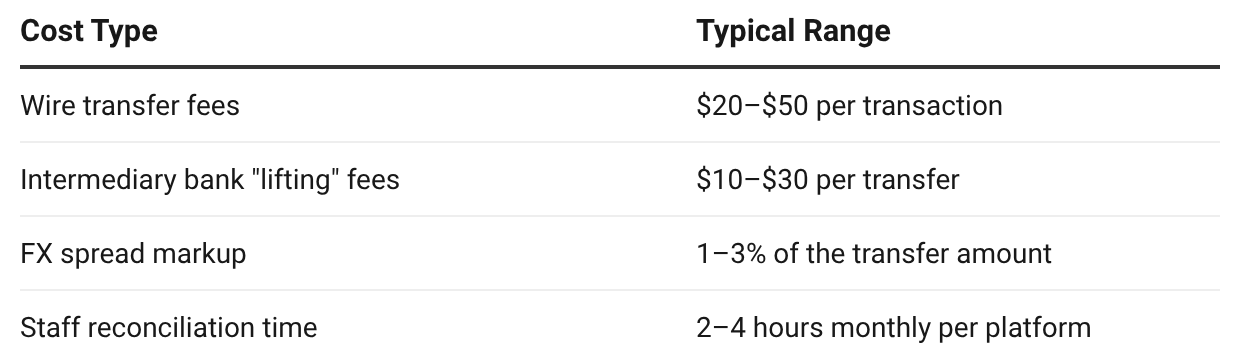

The most visible problem with the lack of strategy is fees. When you’re running payments across multiple platforms, you’re absorbing some combination of:

But the harder problem is that you can’t compare across platforms, which means you can’t tell clients what things actually cost, and you can’t budget for it accurately yourself. Here’s an example to demonstrate:

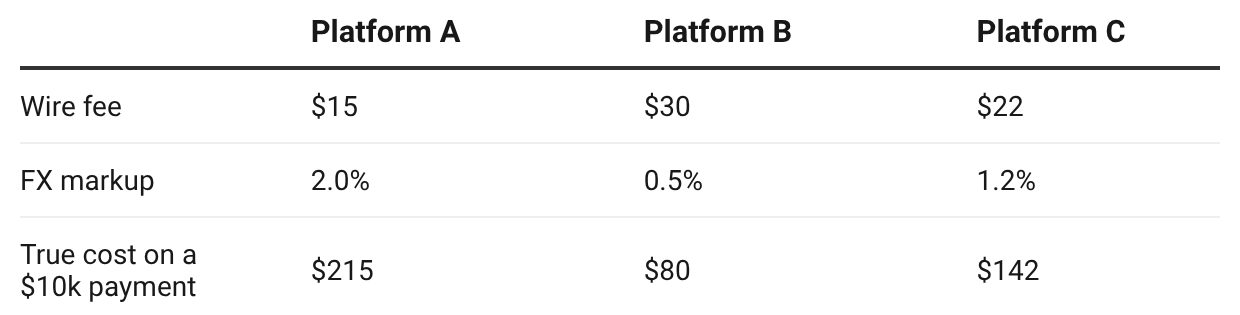

In this example, platform A may look cheapest until you do the math. And nobody’s doing that math every time, which means clients are making payment decisions based on habit, not cost.

The financial hit is only part of it. When payment data lives across multiple platforms, each with different formatting, settlement timing, and exchange rate disclosure, consistency erodes.

That inconsistency doesn’t just create reconciliation work. It:

Weakens reporting clarity

Introduces variability into forecasting

Increases the likelihood of misclassification or incomplete documentation

Over time, fragmented payment processes don’t just cost money. They compromise system integrity, which is the very foundation that advisory confidence depends on.

Evaluate what your setup is really costing you

Whether you’re evaluating your own setup or a client’s, these four metrics tell you if international payments are working or costing more than they should:

1. Total cost per payment: Add up transaction fees, intermediary bank fees, and FX spread markups. If you can’t easily calculate this across platforms, that’s already a problem.

2. Reconciliation hours per month: How much time is spent matching international payments to accounting records? You know manual matching eats hours and takes focus away from higher value work.

3. Payment timing predictability. How much advance notice exists between initiating a payment and when funds actually leave the account? Inconsistency here creates forecasting problems that ripple forward.

4. Cash flow flexibility. Does the current setup allow any control over when funds leave, or does every international payment require immediate outlay? Domestic payments have long offered breathing room between initiation and settlement. FX payments are catching up, and the ability to manage that timing is a lever most clients aren’t using yet.

If any of these are hard to answer, that’s the signal to dig deeper.

Here’s how your international payments could be running

Once firms take a step back and look at the real costs, the next question is inevitable: well, what does a well-structured setup actually look like? The good news is you don’t need to rebuild anything. The capabilities already exist.

Here’s what to look for in the tech:

Everything runs through one platform. Domestic and international, together. That means a consistent audit trail, unified reporting, and no more tab-switching to figure out what a payment actually costs. If you can’t see all your payments in one place, you don’t have a clear picture of your payables - full stop.

Currency conversion happens upfront, not on the vendor’s end. When your client’s vendor is the one absorbing the exchange rate uncertainty, that’s a relationship risk your client may not even know they’re carrying. A better setup converts at the point of transaction, so both sides know exactly what’s moving.

Financing flexibility is built in. This is a real needle mover. At Melio, it’s one of the capabilities we’re most proud of, and consistently one of the most talked about with our clients. International payments can be funded by credit card rather than immediate bank transfer. That means the payment goes out right away, but the cash doesn’t leave your client’s account for up to 45 days. Imagine telling a client: “I can pay your overseas vendor today, but you don’t have to part with the cash for over a month.” For clients managing tight cash flow, that timing can change everything, and it’s the kind of insight that makes clients realize their accountant is thinking about their business, not just their books. Win win.

Clean data, clean books. Every international payment should generate the same clear record: amounts paid, currencies used, exchange rates applied, and settlement dates, and integrate cleanly with your general ledger. If you’re spending hours each month on manual workarounds, that’s a signal the setup isn’t working.

A solution built to scale. The right setup handles five international payments a month the same way it handles fifty, without adding complexity or requiring a new process every time volume grows.

Next time you’re reviewing a client’s payables, ask the question.

How much are they really paying for that overseas wire?

The answer might surprise both of you. The conversations that follow about true cost, cash flow timing and vendor relationships present an advisory opportunity many accountants haven’t tapped yet, because international payments have never been this visible or this manageable before.

The good news is that improving your setup doesn’t mean adding another app to your stack. You get to cut tools rather than accumulate more.

If you’re ready to consolidate your workflow, check out how Melio can help you handle international payments more seamlessly, with you in control.